15 Oct 2025

For many veterinary practice owners, building a successful business has been the culmination of their professional career. This article provides a guide to preparing the practice for sale, ensuring that their hard work and dedication translate into a rewarding exit…

Vicky Robinson

Job Title

Image: AI / Sora

If you are the owner of a veterinary practice, there’s a reasonably high chance that your business and accountancy knowledge is quite low or limited, and there’s a very good reason for that if you’ve dedicated your academic time to veterinary science.

There are, of course, a few high-flying individuals who have come into the profession as non-vet owners, from a business background, have family assistance or have been attracted to learning how veterinary business functions. It struck me many years ago, when we first began our group coaching model and the delegates became relaxed enough to be honest with each other, that non-business orientated owners had an assumption that it was only them with limited knowledge, and that their surrounding “competitors” were all well educated and probably hard-nosed businesspeople making a fortune.

Following that assumption, they might base their fees around those of the local gurus, unknowing that they were all possibly doing the same thing. So, for the purposes of this article, I’m going to assume you aren’t in the high-flying business mogul category and are open to my humble opinions.

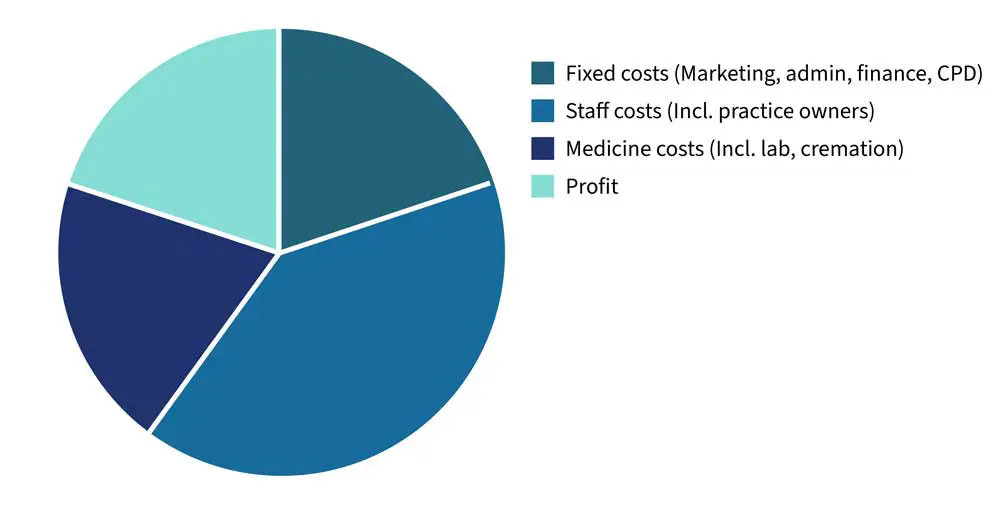

When completing your business plan it’s useful to have a target framework to understand what is realistic and achievable within a veterinary business.

Remember all businesses are unique and this is a basic template, based on a modest 10 per cent profit (from which you need to pay yourself, the tax man and use for reinvestment so you may want to think bigger).

Creating a business plan with a three-to-five-year horizon is a really useful exercise for setting a clear roadmap and having a focus on long-term success. Spend time away from the busyness of work, thinking through what you’d like your practice to be like in the future and getting it down on paper. Challenging your own beliefs and boundaries, and asking opinions of trusted team members, family and/or business advisors, can be the most productive hours you will ever spend on your business.

If the thought of creating a business plan is causing you to eye roll then you wouldn’t be in a minority. However, it might inspire you to know that many owners who had to be “encouraged” to work on their business plan said it gave them structure and a clear understanding of where their business was going.

Many who completed it, but then left it “in a drawer”, said that everything they had written down, including the projected growth, had actually happened when they reviewed their plan years later. Perhaps spending that time creates some universal magic.

Rather than trusting magic, once you have a three or five-year plan, chunking it down and creating three key projects to work on each quarter will ensure you reach your end goal. Doing this with a coach or in a community will encourage you to make it happen – even if it’s the night before your next meeting.

Creating a business plan to maximise your assets and get your business in the right place for you to exit can be highly advantageous to ensure you get the most from your years of hard work.

In an ideal world, the business plan would be in place, work to perfection and you’d get a great deal at your chosen time of exit. As we approach 200 assisted exits, there aren’t many that actually followed that perfect path. In reality (and with the exception of serial entrepreneurs), we don’t normally start a veterinary business with the end in mind.

The end could come quite unexpectedly, life can change, the world can change – the first lockdown triggered multiple exits, and fortunately (financially for the vendors), we were experiencing a corporate buying bubble. If you find yourself without the luxury of planning time, a sale is almost always possible immediately and, of course, depends on the size and profitability of the practice.

Sometimes we might recommend spending a few months making some changes to make the business more sustainable and work on some quick wins to hit the bottom line.

Not many owners are aware of the actual value of their business, and regardless of whether you are interested in an exit, it’s a useful figure to know. Making some adjustments, adding in a salary to replace yourself and any partners, putting in a rental value if not included, your EBITDA (earnings before interest, tax, depreciation and amortisation) can be calculated.

The industry standard multiple of this figure is 4.5 times for a small animal practice, and that is the figure that banks are likely to lend against for a private purchase.

As a coaching company, we offer free valuations to any independent practice owners, or your accountant may provide this service for you, and it’s useful to monitor the value when reviewing your annual business plan.

A slight misconception is that if your business has had recent capital expenditure, maybe for refurbishment, new equipment or a new building or extension, and that year’s trading accounts have taken a dip in profits, then it’s not a good time to sell and better to wait until the following year’s accounts have been produced.

This is absolutely not the case, and any one-off expenses will be removed for valuation purposes – together with any personal expenses as these won’t be necessary for a new owner to run your business.

If the building(s) you trade from are leased from an external landlord, it’s very important you have a suitable lease in place. Most acquirers will want at least a 10-year term; most corporate acquirers prefer a 15-year term.

If the lease is in the name of your limited company then it’s easy to transfer into new ownership. If it’s directly with yourself then a new lease has to be negotiated. If your landlord drags their heels then this will hold up your sale and can be extremely frustrating for all concerned, so tidying this in advance would be time well spent. A normal requirement is that the lease is within the Landlord and Tenant Act 1954, which broadly gives the right to renew at the end of the term.

If you or your pension fund owns the property, you may already have a lease in place with your trading company and charge your business a fair market rent. If you own the property, this makes life easy for sale purposes as you are in control of the lease and your solicitor can work with the acquirer’s solicitor to get an agreeable lease in place. It could be a similar situation if the property is held by a pension fund, depending on the response time from their admin teams.

When beginning the legal section of the sale process, it’s wise to begin working on the lease immediately as any controlling body of your lease is unlikely to have the same sense of urgency around the process as you might, and property matters quite often cause delays.

The Veterinary Landlords Association (VLA) was formed to support and share knowledge. The VLA’s mission is to represent the interests of landlords who lease property to veterinary practices. This not-for-profit association offers mutual support to veterinary landlords to assist them in building good relationships with tenants.

The majority of the members of the VLA have leases in place with a corporate, some with private tenants and some even with themselves.

They have a lively WhatsApp forum where you can quickly get answers from other’s experiences, and they host monthly webinars on related topics.

Their frustration is that landlords join them once they have issues or concerns, and the VLA would like to offer advice to potential sellers.

I asked the VLA for some advice to share with anyone preparing for a sale of their business, as they have extensive amounts of information and knowledge from members experiences over the years.

It’s never too soon to have a plan in place, no matter where your exit horizon is.

There are so many people in the profession who will generously share their knowledge and experience and allow you to learn from their mistakes, so be curious and questioning and access all the help available.

➲ Take professional advice; ascertain what a fair open market rent is by instructing your own surveyor. Leases should be checked by a solicitor who is experienced in the commercial lease market. We always recommend using a solicitor who is well practised in veterinary sales to handle the whole process.

➲ Appreciate that a commercial lease is only secure as long as the first tenants break clause – and the industry standard for this is five years.

As a minimum a lease should contain:

Vicky Robinson had first-hand experience of owning, managing, and growing a highly successful small animal practice for 10 years before she co-founded business consultancy company Vet Dynamics, with husband Alan Robinson MRCVS. Vicky was named winner of Outstanding Female Entrepreneur at the 2019 Best Business Awards and has become a leading broker, helping nearly 200 owners exit their businesses.